Four Growth Paradigms: Zynga, Applovin, Skillz, and Jam City (Part 1 of 2)

As game companies struggle for growth, 4 different strategies for growth are compared

Welcome to another exciting week in the always dynamic and changing F2P gaming industry. 115 GameMakers have joined us since last week! Join this highly exclusive and select group of only 1,121 smart and strategic folks by subscribing here:

🎧 Listen to GameMakers content on Spotify or Apple Podcasts

📺 Watch on Youtube

To All,

The game industry faces structural transition in 2021 as discussed in last week’s newsletter: The Warning | Game Companies Face Structural Transition in 2021. As game companies become desperate for growth, what are the different strategies they will pursue?

Zynga, Applovin, Skillz, and Jam City represent 4 different growth paradigms in F2P gaming. This week I discuss their different approaches to growth and the potential risks these companies face.

Quick summary:

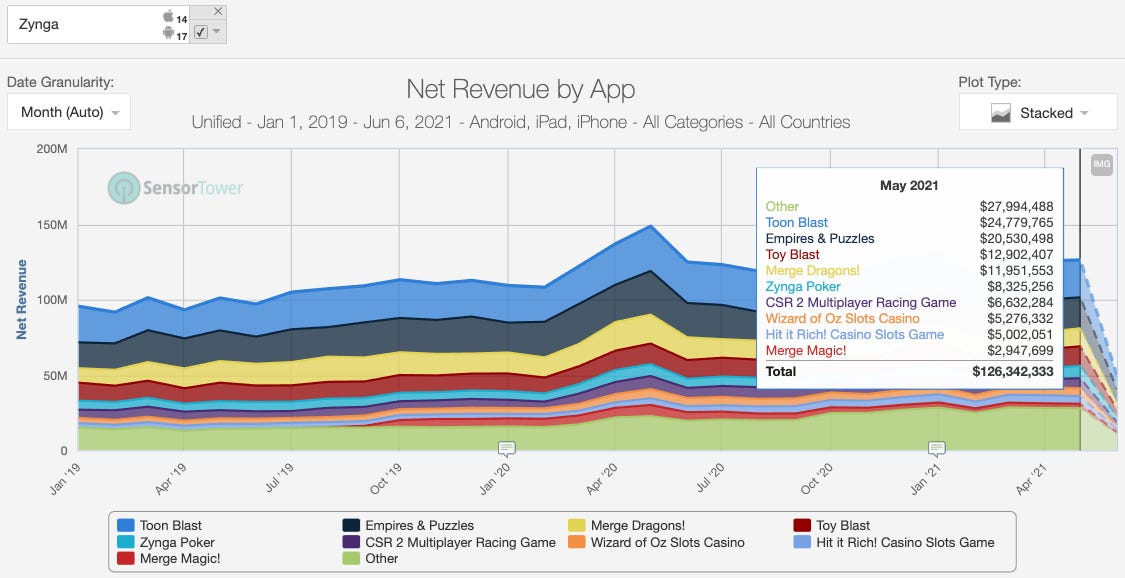

Zynga shifting from content M&A to ads/vertical integration and cross-platform

Applovin is really trying to become the Netflix of Gaming. No, really.

Skillz is “betting on” (get it? lol) building a scaled competitive wagering platform

Jam City appears to be focusing on upstream (earlier stage) content M&A and IP based games

#1. Zynga: End of the M&A Gravy Train

We’re nearing the end of the “easy pickings” phase for game company growth through M&A. Zynga has arguably been the most successful of mobile game companies at leveraging M&A for growth over the past 5 years.

While Zynga has continued to show growth over the past year and likely has growth locked in for the next few years, the big question moving forward is how do they continue growing longer-term?

M&A has been responsible for just about all of its growth over the past 5 years. However, recent moves seem to indicate a strategic shift away from their current model of M&A:

Exec Team: The departure of M&A superstar Chris Petrovic who led Zynga’s massively successful acquisition run over the past 5 years

Shift to Ad-tech: The acquisition of ad network company Chartboost announced last month for $250M

Shift to Cross-platform: The acquisition of Echtra Games to expand cross-platform capabilities. Announcement of new Zynga Star Wars: Hunters game as cross-platform to mobile and Switch.

In my view, the Zynga executive team saw the writing on the wall for continued growth through mobile game content via M&A and decided to follow Applovin into ad tech. Further, they also realized the potential for cross-platform given the success of Genshin Impact.

More recently, disclosures from the Epic vs. Apple Trial have also highlighted the market potential of F2P on the console platform relative to mobile. In particular, a lot of chatter from game executives about the slide below showing Fortnite revenue share by platform. For Fortnite from March 2018 - July 2020 that would be 7.5% mobile to 92.5% for PC/Console:

By the way, you should take away that console poses a very strong opportunity for F2P games. However, also note with respect to the chart above that console contribution is a bit overstated:

On Android, Fortnite's Android launch was delayed and then only on Samsung. Further, Epic opted to go with their own launcher which had massive friction given Google’s restrictions.

iOS launch at that time required super high device requirements, not to mention an even bleaker picture for device support on the Android side. Of the top 100 grossing mobile games on iOS at that time, Fortnite was #100 out of 100 in terms of device spec requirements.

Zynga Outlook

Just to be clear, I’m not a hater. While I wasn’t a huge fan of Zynga pre-Frank Gibeau, I’ve publicly commented very positively on Zynga over the past few years on podcasts and to other game industry folks.

Having said that, Zynga is clearly shifting its high-level growth strategy. Anytime a management team adopts a completely different strategy, there will be some execution and market risk. Given that, while I remain positive about Zynga’s growth over the next couple of years or so, I think medium to long-term Zynga will be challenged.

Just think if Zynga weren’t able to find the next Peak or Small Giant:

A few thoughts on their 2 growth vectors of Ad Tech Vertical Integration and Cross-Platform.

Ad Tech Vertical Integration

My belief is that Zynga is opportunistically following this path largely based on copycatting Applovin, but is one step behind.

Comments from Zynga’s management team seem a bit confused and not consistent in terms of approach or how this will work. Will they do a walled garden or will they do an open ad network?

If I’m being honest, I also don’t think Zynga has a very specific point of view on how to specifically address IDFA deprecation. This is fair since we’re still finding out more about the impact of IDFA deprecation, but a little concerning that Zynga’s sort of “winging it” here (if my assumption of Zynga is correct on this).

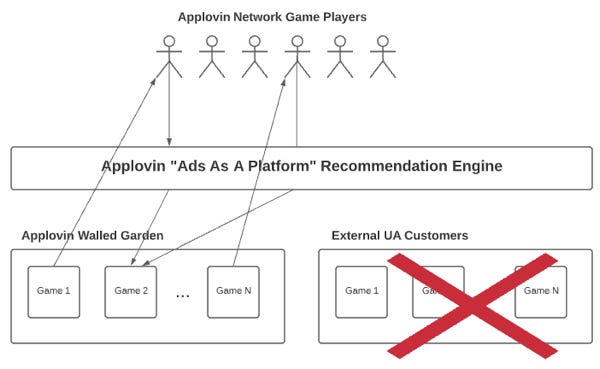

Note that while Zynga followed Applovin down this growth path, they seem to have a fundamentally different approach to this business model. It would appear that while Applovin will likely go for a walled garden “Netflix of Gaming” approach (see below), Zynga is indicating they want to try to have the best of all worlds by capturing additional margin from owning ads and having an open ad network in which competitors will gladly give them their data and trust them not to abuse that trust.

This growth vector fundamentally holds the most risk. Game studios are becoming increasingly wary of sharing data with compromised ad networks and the competitive advantage from owning ad tech/ad network data (e.g., Auto ROAS) doesn’t seem to be panning out as much as originally hoped (if the current rumors are correct).

#2. Applovin: The Netflix of Gaming

According to Applovin CEO Adam Foroughi:

That first-party data feeds our software, and then creates the ability for us to be much better at recommending future content to customers … I guess maybe the best analogy to really compare that to is how Netflix took their own data on their platform and rolled out personalized recommendations ... then they layered on their own original content, which exploded the amount of consumption on their platform and gave them more insights into their audience — replicating that same playbook in a new media format.

Taken on the face of it, a true “Netflix of Gaming” approach means that Applovin is viewing ads as their Netflix-style recommendation platform. This is a concept with implications that a lot of folks just don’t seem to understand so let me explain:

In the current scenario, Applovin serves ads in its owned and partner properties. They have applied a shit ton of data analysis and machine learning to optimize recommendations and predictions on ad serving. This is very much an “Ads-as-a-platform” recommendation engine. From the Applovin S-1 filing:

Our Core Technologies are robust, having processed over 3 petabytes of data per day on average, as many as 3 trillion predictions per day, and up to 6.5 trillion events per day in January 2021, while remaining flexible enough to rapidly adjust to our customers’ evolving needs. Our App Graph stores and manages anonymized data from hundreds of millions of mobile devices we reach every day, which our AXON engine then leverages to better predict and match each user to relevant advertising content.

Let’s get to the crux of the business model discussion now: In a Netflix of Gaming model, does it make sense for Netflix to recommend content on competitive services like Amazon or HBO?

I believe that Applovin has been preparing the public for their shift to a fully walled garden Netflix-style business model. Even by revenue break-out, they have separated their sources of revenue to support this model:

Here:

Business revenue: “fees paid by mobile app advertisers, or business clients, that use our Software to grow and monetize their apps.”

Consumer revenue: “when a user of one of our Apps makes an in-app purchase (IAP).”

Note Applovin did not break out revenue by games as a vertical in which they would more naturally consolidate all of the revenue generated by the games business together

An important point to make: Based on revenue, many people who simply call Applovin a “gaming company” fundamentally miss the whole point of Applovin’s strategy. So while a big chunk of ad revenue classified in “Business revenue” may come from Applovin owned games, the question people fail to realize is: What happens to Business Revenue when Applovin shifts to a walled garden?

Business revenue could go to zero, or monetize only against non-competitive games.

Revenue should flow from Business to Consumer Revenue through higher margins

Now while I’m sure Applovin is likely going to try to hold on to external gaming customers for the ad business I don’t think they are counting on it. I discussed one of the initiatives I believe they are working on last week - Auto ROAS - which would create a very compelling product proposition for external customers despite the competitive risk.

However, we are seeing some activities which tend to indicate to me that Applovin may not care to lose the external customer business.

Case in point: The continuation of competitive behavior on the games side of their business. Note the recent launch of “Life Simulator: Best Life” which happens to be very similar to the game “BitLife: Life Simulator” by Max (mediation) and Applovin (ad network) customer CandyWriter/Stillfront.

BitLife: Life Simulator

VS.

Life Simulator: Best Life

Applovin Outlook

Applovin likely has the smartest, most aggressive, and execution capable executive team in the F2P games industry. Despite the huge vision and difficulty behind a Netflix of Gaming model, it’s not wise to count them out.

While valuation is a separate issue, from a content perspective Applovin’s biggest challenge will be transitioning from having a core competency in ad tech to content development and managing studios. Netflix made a similar transition from logistics and infrastructure to streaming and content development.

So while I think, they have as big or even more of a challenge than Zynga, I’ve learned it’s not wise to bet against a ruthlessly executing management team like Applovin’s.

Keep an eye out for:

The evolution of walled garden vs. open approach to their ad tech business. In particular, watch the shift in Consumer vs. Business Revenue.

Applovin’s ability to execute against an Auto ROAS capability

Applovin’s moves to develop content development capability in the form of 1. additional executive team hires and 2. additional studios and genre expansion/capability

(To be continued on Wednesday. Stay tuned!)

Hey folks,

I coincidentally publish a stock investment Youtube series called Super Stonk Bros (with co-host Steve Palley and sometimes with Bloomberg’s Matthew Kanterman). We coincidentally covered the companies covered in this newsletter there with a focus on investment potential and I provide links below:

Zynga:

Applovin:

LILA Games is building one of the most ambitious shooter games ever designed! We are currently hiring aggressively in Bangalore, India. See below.

Visit our website!

LILA Openings (Bangalore or Remote):

LILA Openings (Bangalore Only):